Riyadh and Dubai do represent two fundamentally distinct real estate investment models, differentiated by their demographic compositions and resulting risk-return characteristics.

Permanent citizen populations generate predictable, compounding housing demand with lower volatility, while expatriate-dependent populations create higher growth potential coupled with cyclical sensitivity to economic shocks.

● Permanent residents generate long term, cumulative demand that is less sensitive to cycles.

● Residents tied to the labor market translate into cyclical demand that expands quickly and contracts just as fast.

Bottom line: Demographics here shift from being a descriptive population metric to becoming a risk and pricing factor.

Riyadh's projected 4.1 million Saudi citizens by 2030 will drive demand for 305,000 new housing units through 2034, underpinned by household formation and homeownership rates rising from 65.4% to 70%.

Property prices grew 10.6% in Q2 2025, supported by demand from nationals with permanent residency status. This demographic permanence establishes minimum occupancy levels that persist across economic cycles.

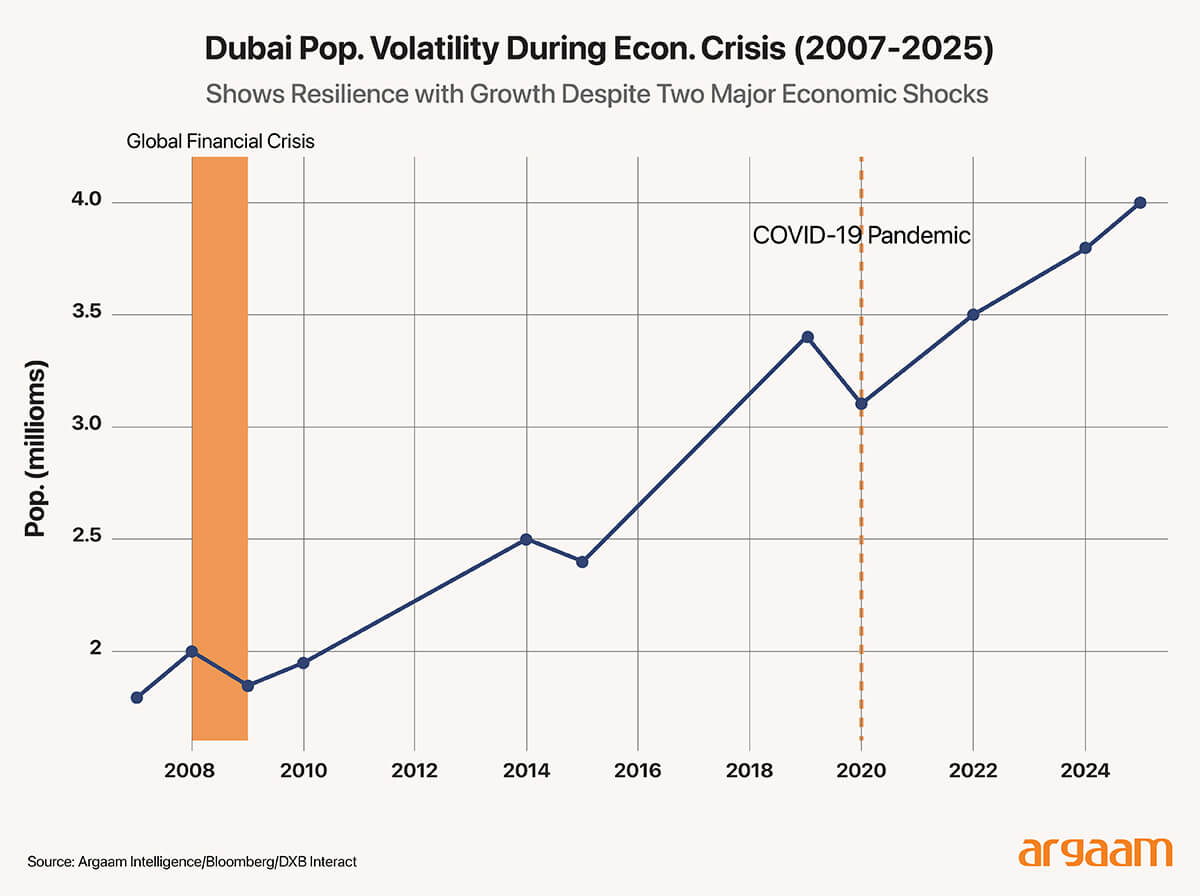

On the other hand, Dubai's demographic composition—3.7 million expatriate workers (92% of population) against 300,000 Emirati citizens—creates a distinct risk-return profile characterized by higher volatility.

Property prices declined 50-60% during the 2008-09 financial crisis, then recovered with 70% appreciation between 2021-2024.

The 2020 pandemic triggered an 8.4% decline in population, the steepest in the Arabian Gulf region. Fitch Ratings projected a 15% price correction in 2025, consistent with the cyclical pattern characterizing Dubai's real estate.

For investors across 10-20 year horizons, the key distinction centers on risk tolerance and return objectives: Riyadh's citizen-based model offers demographic stability, where annual population growth adds irreversibly to the base, creating compounding demand.

Dubai's expatriate-dependent model offers higher peak returns during expansion phases, coupled with population volatility where residents arrive during booms and depart during downturns.

Investment selection depends on whether capital preservation with moderate growth, or cyclical opportunities with higher volatility, better align with portfolio objectives.

Permanent Citizens vs Transient expatriates

The fundamental distinction between Riyadh and Dubai real estate markets originates from the immutable demographic composition of each city's population base.

Riyadh's growth trajectory centers on a substantial and expanding Saudi citizen population with generational housing needs.

On the other hand, Dubai's expansion model leverages temporary expatriate workers whose residency permits tie directly to employment contracts, creating distinct demand characteristics.

Riyadh's 2022 census recorded 7 million total population - comprising 3.35 million Saudi citizens and 3.66 million expatriate workers.

By 2030, it’s projected that the city will reach 9.6 million residents, with Saudi citizens growing to 4.1 million and expatriates to 5.5 million.

This represents a 750,000 increase in permanent citizen population over eight years—individuals with lifelong housing requirements and family formation patterns that drive multi-decade demand.

Dubai's demographic structure follows a different model. As of 2025, Dubai's 4 million population comprises approximately 300,000 Emirati citizens—7.5% of total residents—against 3.7 million expatriates representing 92.5% of all inhabitants.

This expatriate majority holds temporary residency tied to employer sponsorship, with no pathway to citizenship. Economic contractions trigger employment losses and residency permit expirations within 30-60 days, directly impacting housing demand.

The implications for housing demand sustainability reflect these structural differences. Riyadh's growing citizen base generates permanent demand that compounds annually through natural population growth, marriage, household formation, and generational wealth transfer. This creates minimum occupancy levels that persist across economic conditions.

Dubai's expatriate composition creates demand characteristics tied to economic cycles. During expansions, expatriates migrate to Dubai seeking employment, driving population growth.

Economic contractions—triggered by regional geopolitics, oil price volatility, or global recessions affecting trade activity—reverse this pattern. When expatriates depart, vacancy rates increase, rental yields decline, and capital values adjust until the next expansion cycle.

The Non-Cyclical Backbone of Saudi Real Estate Investments

Knight Frank projects demand for 220,000 new housing units from Saudi nationals between 2024 and 2030, rising to 305,000 units through 2034.

This demand calculation incorporates Saudi Arabia's marriage patterns, where household formation occurs primarily through marriage of young adults entering prime marriage age (25-35 years old) over the next decade.

Saudi Arabia's homeownership rate stood at 47% in 2016, rising to 65.4% by 2024—an 18.4% point increase over eight years, driven by mortgage lending growth and land grant programs.

In 2024 alone, over 122,000 Saudi families benefited from housing support. Total residential lending reached SAR 859 billion ($229 billion) by end-2024.

● Rising vacancies within specific segments rather than the market as a whole.

● A slowdown in new lease contracts relative to renewals.

● A shift in demand from buying to renting.

● An acceleration in supply deliveries alongside a slowdown in net migration.

Government-related entities have announced projects expected to add approximately 330,000 housing units to Riyadh's housing stock by 2030.

However, this supply pipeline faces potential delays due to construction capacity constraints, land costs, and material price inflation, creating conditions where demand growth may outpace actual unit deliveries.

The average apartment prices in Riyadh rose 10.6% y/y in Q2 2025 to reach SAR 6,175 per square meter, with prime districts like Al Taawun recording 32% y/y price rises.

Despite large-scale developments, Saudi Arabia faces a housing shortfall of 1.5 million units nationwide.

Knight Frank estimates over 115,000 housing units need to be built annually until 2030 to meet demand from Saudi nationals alone, yet actual construction delivery rates fall short. This structural undersupply creates potential for sustained price appreciation.

This demand derives entirely from permanent citizens whose housing needs persist across economic cycles. Saudi families require housing regardless of economic conditions, creating what economists term as"non-cyclical demand"—where occupancy rates and rental yields demonstrate lower volatility during recessions.

This demographic stability positions real estate investments with characteristics resembling quasi-bonds with embedded growth optionality; namely, bonds typically offer fixed income, security, and predictable returns.

Dubai's expat-driven model

Dubai's real estate market has experienced three major correction cycles since 2008, each triggered by external economic shocks that caused expatriate population declines and property price adjustments.

These historical episodes demonstrate the cyclical characteristics inherent in expatriate-dependent markets.

The 2008-09 global financial crisis marked Dubai's first modern real estate correction. Property prices peaked at approximately $4,500 per square meter in 2008, before declining by 50-60% to $2,500 per square meter by 2011.

Research notes that simple counting of lights in apartment buildings at night revealed low occupancy rates, with some communities experiencing significant vacancy.

Nearly 40,000 unfinished units faced financing challenges, as investors adjusted to secondary market prices below initial purchase prices.

The 2020 COVID-19 pandemic triggered Dubai's third population adjustment within 12 years. Dubai's population declined 8.4% in 2020, the steepest decrease in the Gulf region - according to S&P Global Ratings.

Oxford Economics estimated the UAE could experience 900,000 job losses among a population of under 10 million—representing 10% of total residents. This departure pattern translated into rental income adjustments, vacancy increases, and price corrections.

Importnatly, Dubai's recovery from COVID-19 demonstrates the market's cyclical nature. Between 2021 and 2024, property prices surged approximately 70%, reaching record levels of $5,000 per square meter.

Yet Fitch Ratings' 2025 analysis projects this expansion has matured, forecasting a 15% price correction. This cyclical pattern typically stems from external global events.

● Credit tightening / higher interest rates

● A heavy wave of deliveries over the next 12–18 months

Investors purchasing at cycle peaks historically experienced capital value declines that require 5-7 years to recover. The key question here centers not on whether Dubai will experience future corrections—historical patterns suggest cyclicality persists—but on timing trigger events and magnitude of adjustments.

Compounding vs amplification

The global investment community frequently applies uniform analytical frameworks to GCC real estate markets, potentially undervaluing the demographic distinction between citizen-based and expatriate-dependent models.

This analytical gap creates opportunities for investors who understand how permanent populations compound housing demand, while transient populations amplify economic cycles.

Riyadh's citizen population growth compounds annually—each year's population increase adds to the previous year's base, creating exponential growth in cumulative housing demand over decades.

A Saudi family purchasing a home in 2025 generates demand extending 50-80 years as the property transfers through generations.

This generational continuity creates what is characterized as "annuity-like cash flows"—predictable, long-duration income streams that justify valuations based on lower discount rates.

Conversely, Dubai's expatriate population growth amplifies economic cycles rather than creating compounding demand. When 200,000 new expatriates arrive during an expansion year, they generate immediate housing demand—but this demand remains contingent on continued employment.

Economic reversals enable these same 200,000 residents to depart within months, eliminating their housing demand. Unlike population growth of citizens that compounds irreversibly, expatriate growth amplifies current economic conditions without creating long-term structural demand.

Analysts evaluating GCC markets sometimes apply frameworks developed for London, New York, or Singapore—cities where residents relocate between neighbourhoods but do remain within the country during recessions.

These frameworks require adaptation for Dubai because the resident base can relocate internationally, not merely domestically. Market pricing reveals potential mispricing relative to demographic risk differences.

If Dubai properties incorporated risk premiums reflecting expatriate volatility, prices would theoretically trade at discounts to Riyadh properties after adjusting for quality and location.

In reality, prime Dubai properties trade at $3,600-7,000 per square meter while Riyadh properties trade at $1,200-2,500 per square meter. This price differential primarily reflects amenity and infrastructure differences rather than demographic risk premiums—suggesting potential opportunities for investors who incorporate demographic risk into valuation models.

Forward-looking indicators for monitoring these dynamics include several metrics. Homeownership rate progression will validate conversion of demographic demand into actual buying of residential property.

Future economic contractions will test whether Dubai's recent economic diversification efforts have structurally reduced expatriate volatility or temporarily delayed cyclical patterns.

In the case of Riyadh, the foreign ownership reform (effective January 21, 2026) will test whether international investor interest translates into capital inflows necessary for institutional-scale market development.

The insight here centers on a fundamental distinction: real estate investment returns over multi-decade periods correlate more strongly with demographic inevitabilities than policy initiatives.

Governments can announce development projects and reform regulations, but they cannot prevent expatriate departures during crises, nor can they eliminate permanent citizens' lifelong housing requirements.

Powered by Froala Editor